Business Succession Planning for Incorporated Owners

Image Source: Gemini 2026

Incorporated business owners hold significant wealth inside private corporations that can’t be transferred without careful tax and estate planning. A coordinated business succession plan addresses capital gains exposure, corporate structure, insurance, and wealth extraction years in advance to protect the value you’ve built.

You built your business from the ground up. The retained earnings, the corporate structure, and the client relationships that took years to earn. At some point, every incorporated business owner arrives at the same question: “What happens to all this when I decide to step back?”

Business succession planning is where that question gets answered, but not in the way most people expect. It’s not a single document you sign and file away.

For incorporated business owners, succession is a multi-year wealth strategy that touches every layer of your financial life: corporate tax planning, estate planning, insurance, and the extraction of wealth accumulated over decades in your corporation.

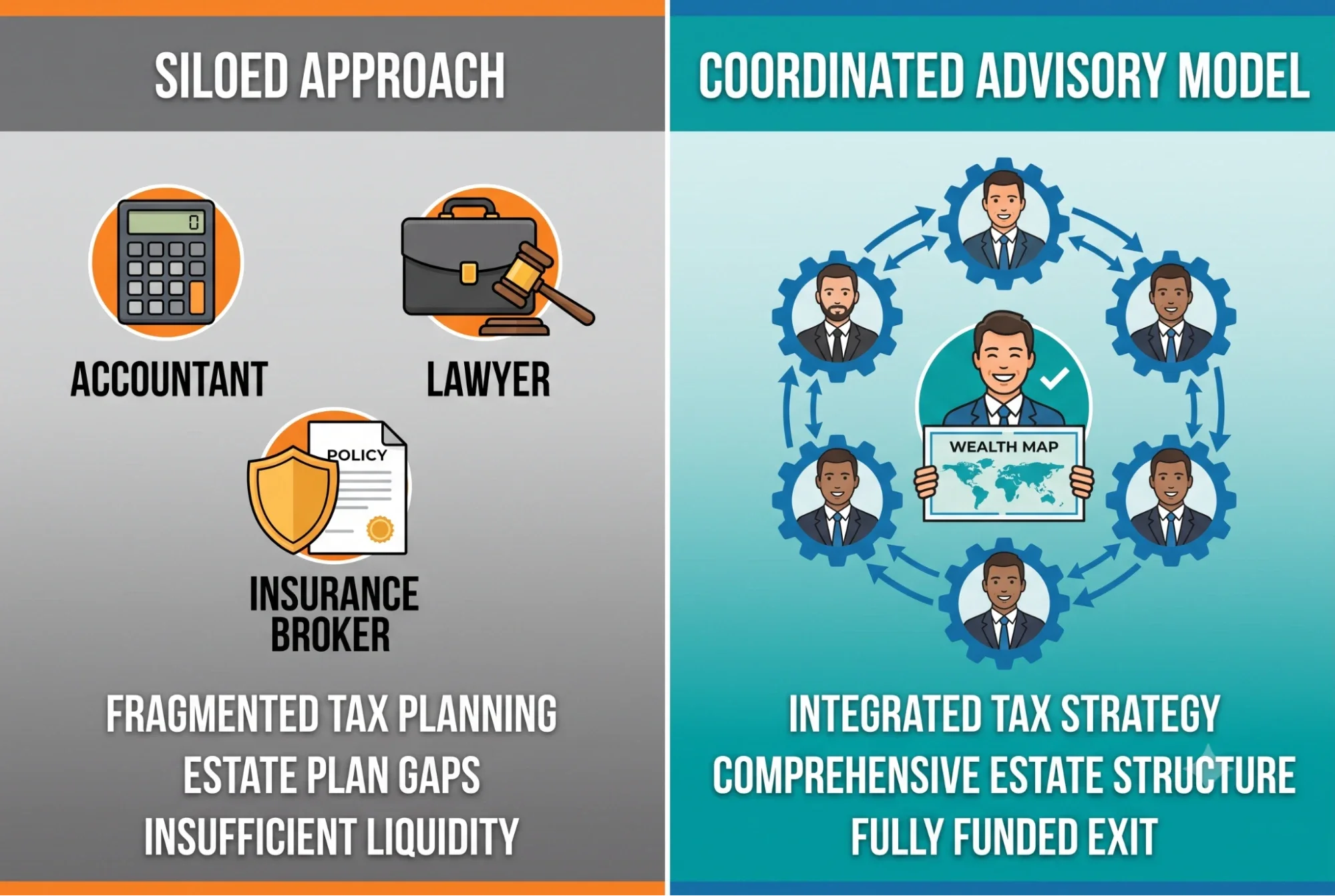

If you’ve been managing your affairs through a patchwork of separate professionals, a corporate accountant here, an insurance broker there, a financial planner at your bank, succession planning is the moment where that siloed approach starts to cost you.

According to MNP, two-thirds of Canadian business owners lack a written succession plan, and only 9% have a formal one. Getting this right requires coordination, not just competence.

Why Incorporated Owners Face a Different Succession Challenge

An incorporated business owner has a fundamentally different wealth profile than a salaried professional or a C-suite executive at a public company. Your wealth isn’t sitting in a personal investment account. It’s held inside a private corporation, in retained earnings, in goodwill, in business assets that can’t simply be transferred or liquidated without significant tax implications.

Incorporating your business creates a distinct legal and tax entity separate from you as an individual. That separation is enormously advantageous while you’re building. When it comes time to exit, it introduces a dual financial identity that most generalist advisors aren’t equipped to navigate: you’re simultaneously the shareholder who owns the asset and, in most cases, the operator who has been running it.

A business succession plan for an incorporated owner isn’t just about finding a buyer or grooming a successor. It’s about structuring the transition so that the wealth you’ve spent years building inside that corporation reaches you, and eventually your family members, in the most tax-efficient manner possible.

Source: Canva

The Wealth Held Inside Your Corporation

Retained earnings inside a Canadian private corporation are taxed at a low corporate rate while they remain inside the active business. The moment they’re extracted, whether through salary, dividends, or a sale, income tax and potentially capital gains tax apply.

For many business owners, the gap between a business's fair market value and its after-tax exit proceeds is a genuine shock.

Anticipating the gap between business value and actual proceeds requires years of planning. Strategic tools such as estate freezes, holding company structures, and the lifetime capital gains exemption are not quick fixes; they’re long-term maneuvers that demand careful coordination.

When implemented too close to a business exit, their effectiveness drops sharply. However, with an advisor who has years rather than months to prepare, the associated capital gains and tax liabilities become significantly more manageable.

Why the Timeline Matters More Than You Think

The most common mistake in succession planning is starting too late. A runway of three to five years is the baseline required to establish the structural protections your business value demands, rather than an aggressive timeline.

Currently, 61% of SMB owners have reached age 50, and two-thirds intend to exit their companies in the next five years. Despite these intentions, fewer than one in three Canadian family enterprises successfully transition to the second generation. For those who view succession as a distant concern, these statistics highlight a significant risk to their legacy.

An estate freeze locks in the current fair market value of your shares and transfers future growth to the next generation or a holding entity. Done early, it’s one of the most powerful tools in Canadian corporate estate planning. Done in the year before a sale, its value is sharply limited.

The same applies to corporate-owned life insurance (COLI), which can serve as a tax-efficient vehicle for wealth transfer and liquidity when integrated into a succession and estate planning strategy from the outset.

Source: Canva

The Components of a Coordinated Succession Strategy

Proper estate and business succession planning at this level requires a coordinated set of decisions across legal, tax, insurance, and investment dimensions that must move together. Here’s what a well-structured plan addresses.

Corporate Tax Planning and Wealth Extraction

How you extract value from your corporation during the transition period directly impacts your personal net worth and your tax obligations for the taxation year in which the transaction occurs. The right mix of salary, dividends, and shareholder loans depends on your income needs, your marginal income tax rate, and the structure of any pending transaction.

Strategic tools, such as a registered retirement savings plan (RRSP) or an individual pension plan (IPP), are integral to an effective extraction strategy. By sheltering transition-period income, these instruments help lower your total tax liability.

Additionally, implementing income splitting via a family trust can further minimize tax burdens, provided the structure is established early enough to meet CRA standards.

A coordinated approach to corporate tax planning means these decisions aren’t made in isolation. Your extraction strategy, your estate planning goals, and your investment portfolio all interact, and optimizing one without visibility into the others is how business owners leave significant value on the table.

Estate Planning and Multiple Wills

The estate planning process for incorporated business owners is far more complex than that for a standard will. Private corporations create specific exposure to probate fees that can be significantly minimized through a strategically structured estate.

A proven approach in Canadian corporate estate planning involves creating multiple wills: one for assets requiring probate and another for private corporation shares that don’t, thereby shielding a substantial portion of the estate from avoidable fees.

Effective estate planning also addresses deemed disposition, a process in which the CRA treats your assets as sold at fair market value upon your death. For owners of incorporated businesses, this often results in significant capital gains taxes on corporate shares. Implementing a strategic plan allows you to mitigate these tax liabilities in advance, protecting your estate from avoidable financial burdens.

While it’s critical to review your estate planning every three to five years, certain milestones require more immediate attention. To ensure your strategy remains effective, an instant update should be triggered by significant life or business events, including:

The sale of business assets or interests

A corporate restructuring

Modifying a shareholders' agreement to include key employees

Image Source: Gemini 2026

Insurance, Key Employees, and Business Continuity

Rather than being an isolated discussion, insurance should be central to the succession strategy for incorporated business owners.

Using corporate-owned life insurance (COLI) can effectively fund buy-sell agreements, provide vital estate liquidity, or serve as a tax-efficient accumulation tool within the company.

Furthermore, securing policies for key personnel safeguards the organization against financial instability caused by unexpected health crises or departures during a leadership change.

A shareholders' agreement that addresses buyout provisions, decision-making authority, and the transfer of shares to family members or new leadership is a critical piece of any succession plan. Without it, achieving a smooth transition becomes significantly harder, and employees and clients may lose confidence in the business amid the uncertainty.

Family Dynamics and Transparent Communication

Many business owners underestimate the extent to which family dynamics shape the succession process. When a family business is involved, the stakes extend beyond tax efficiency into family harmony, perceived fairness, and the transfer of institutional knowledge to the next generation.

Regular family meetings create a structure for transparent communication about succession plans, who’s involved in the business, what roles they will take on, and how decision-making authority will transition over time.

Critical knowledge transfer doesn’t happen automatically; it requires deliberate planning and enough lead time for new leadership to develop the necessary skills. Formalizing that process is key to ensuring the business continues to run smoothly after the transition.

Source: Canva

What Gets Lost When Advice Is Siloed

Most incorporated business owners don’t lack professional relationships. They have accountants, lawyers, insurance brokers, and financial planners. The problem is that these professionals rarely talk to each other, and the cost of that silence shows up in succession and estate planning more than anywhere else.

When your accountant structures a corporate sale without visibility into your estate plan, or your insurance broker recommends a COLI policy without knowing your extraction timeline, the result is a set of well-intentioned decisions that do not add up to a coherent strategy. Tax considerations get addressed in pieces rather than as a whole.

You end up coordinating yourself, translating between tax professionals who each hold one piece of the picture.

That’s the problem a truly integrated advisory model is designed to solve. When tax strategy, insurance, investing, and estate planning are coordinated under one roof, with a dedicated advisor who sits next to you, not across from you, business succession planning becomes what it should be: a deliberate, multi-year strategy that protects what you have built and positions you for what comes next.

FAQs About Business Succession Planning

-

Business succession planning is the process of structuring the transfer of a privately held corporation in a tax-efficient manner. For incorporated owners, it covers wealth extraction, estate planning, corporate restructuring, insurance, and the transfer of shares to family members or new leadership.

-

Starting too late. Most business owners begin planning within a year or two of their exit, leaving insufficient time to implement estate freezes, shareholder agreements, and tax strategies that require years of lead time to deliver full value.

-

Incorporated owners face deemed disposition, capital gains exposure on corporate shares, and probate fees on business assets. Multiple wills, holding company structures, and COLI can significantly reduce these liabilities, but only when integrated into a proper estate planning strategy well in advance.

-

At least three to five years before any planned exit. Many business owners wait too long, limiting their options for tax-efficient wealth extraction, capital gains exemptions, and a smooth transition to the next generation or new leadership.

Key Takeaways

Business succession planning for incorporated owners is a multi-year wealth strategy, not a one-time transaction.

Wealth held in a private corporation is subject to income and capital gains taxes upon extraction, but proper planning can minimize both.

Tools like estate freezes, multiple wills, and corporate-owned life insurance (COLI) must be implemented years before an exit to be effective.

A clear estate plan addresses deemed disposition, probate fees, and intergenerational wealth transfer before they become costly surprises.

Siloed advice from separate tax professionals, lawyers, and insurance brokers creates gaps, but a coordinated advisory model closes them.

Two-thirds of Canadian business owners lack a written succession plan. Starting early is the single most impactful decision you can make.

The Right Time to Start Is Before You Think You Need To

If you’re beginning to think about stepping back, even loosely, even years from now, that’s the signal to start planning.

The business owners who navigate succession most successfully treat it as a wealth strategy from the outset, not a transaction to be managed at the end. Advance planning isn’t just good practice for your financial future; for incorporated owners with complex corporate structures, it’s the difference between a tax-efficient exit and a costly one.

Longevity Wealth works with incorporated business owners across Canada to build coordinated, advisor-led business succession planning strategies that address the full complexity of their financial affairs, from corporate tax planning to estate structure to insurance and beyond.

Our 360-degree advisory model means your dedicated advisor understands every dimension of your situation, and the professionals around them are working from the same plan.

Book a no-obligation discovery call to start the conversation. There’s no better time to plan for what you’ve worked this hard to build.