Executive Compensation, Decoded

Image Source: Pexels

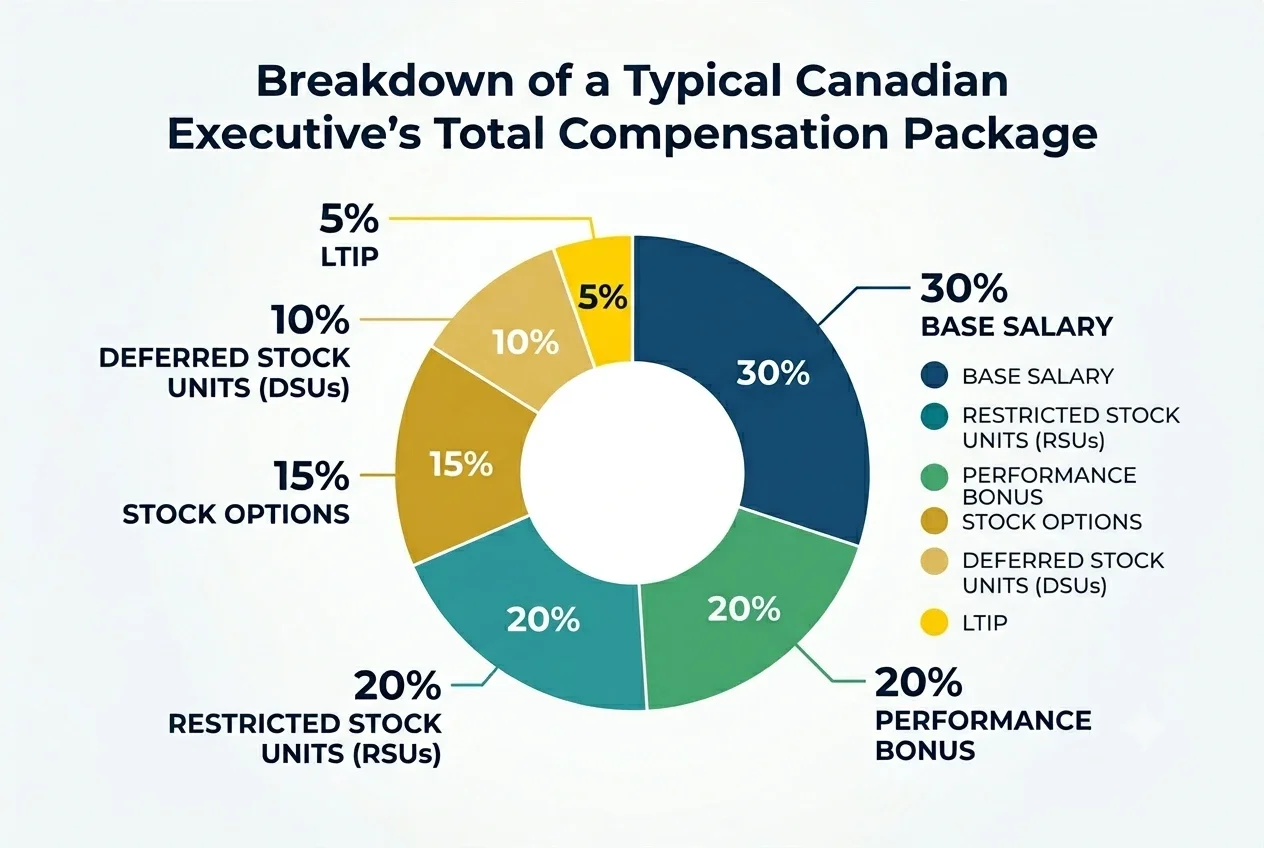

Canadian C-suite executives manage compensation packages that extend well beyond salary, including RSUs, DSUs, and LTIPs, each with distinct tax implications. Coordinating deferred executive compensation timing, RRSP and IPP contributions, income splitting strategies, and capital gains planning can significantly reduce taxable income and build long-term wealth.

Your Salary Is the Simplest Part

If you’re a Canadian C-suite executive, your paycheque is only the tip of the iceberg.

Between restricted stock units (RSUs), deferred stock units (DSUs), stock options, and long-term incentive plans (LTIPs), your compensation is likely spread across several moving parts, each with its own tax rules, timelines, and planning opportunities.

When all of that collides with Canada’s top tax brackets, the difference between “do nothing” and “plan carefully” can be hundreds of thousands of dollars over your career.

The real complexity typically sits around it in the form of:

Long-term incentive plans (LTIPs): Ties a portion of the executive pay to performance or tenure targets over a multi-year period

Restricted stock units (RSUs): A promise of company shares delivered once a defined vesting schedule, whether time or performance-based, is met.

Deferred stock units (DSUs): Notional units that track share value and pay out only in retirement or upon leaving the company, deferring tax.

Phantom equity: A contractual right to cash tied to share appreciation, without issuing actual equity or diluting existing shareholders.

Performance-based bonuses: Variable cash payments tied to hitting specific business targets, arriving outside a predictable pay cycle.

Each of these comes with:

its own tax treatment

a specific vesting or payout timeline

a window where planning is most effective

When those shares vest or those options pay out, it can be tempting to treat them as a windfall. That is one of the most expensive habits a newly promoted executive can develop.

Source: Canva

The Tax Problem No One Warns You About

Executive compensation is, at its core, a tax problem.

When RSUs vest or stock options are exercised, the resulting value is typically treated as employment income in Canada. For many executives, that’s enough to push them firmly into the highest tax bracket.

Without a strategy in place, a large portion of that gain disappears before it ever has the chance to grow in your portfolio.

Deferred compensation arrangements, such as DSUs and certain LTIP designs, give you real control over when that income is recognized and when tax is triggered. With the right plan, you can align this income with:

lower-income years

a period after a major liquidity event

Registered retirement savings plans (RRSPs) remain one of the most effective tools available to Canadian executives. A contribution room built up during high-income years can shelter investment growth from tax and also reduce the tax rate applied to your other income sources in the same year.

For executives with a longer planning horizon, an Individual pension plan (IPP) can go even further. IPPs often allow larger contributions than an RRSP, making them one of the more powerful tax-deferral structures available to high-net-worth Canadians.

Equity Concentration Is a Risk, Not a Reward

Many executives accumulate substantial employer equity over time. What begins as an incentive becomes a concentration risk: a large portion of net worth tied to a single company's performance, with capital gains tax consequences attached to any move toward diversification.

A tax-efficient approach to diversification weighs the capital gains triggered by selling vested equity against the cost of holding a concentrated position. Tax-loss harvesting elsewhere in the portfolio can help offset capital gains in certain scenarios, and donating appreciated securities directly to a donor-advised fund can eliminate capital gains tax entirely while generating charitable tax credits that reduce your overall tax bill.

These aren’t simple calculations. They require a financial advisor who understands both the compensation structure and the broader wealth picture.

Income Splitting and Family Tax Planning

For executives with a spouse or other adult family members, income-splitting strategies can meaningfully reduce the household’s overall tax burden. Prescribed rate loans allow investment income to be shifted to family members in a lower tax bracket, reducing the tax rate applied to that income at the household level.

Spousal RRSP contributions serve a similar function, building retirement assets in the lower-earning spouse's name to support more tax-efficient withdrawals later.

These strategies must be structured carefully. The Tax on Split Income (TOSI) rules limit certain income-splitting arrangements, and the planning must withstand CRA scrutiny. Working with a qualified tax advisor alongside your financial advisor is essential.

Image Source: Gemini 2026

FAQs About Executive Compensation

-

Executive compensation refers to the total financial payments and non-monetary benefits provided to senior corporate officers, including base salary, performance bonuses, equity-based incentives such as RSUs and stock options, deferred compensation, and other executive benefits.

-

High-income earners in Canada can minimize taxes through RRSP and IPP contributions, deferring compensation, income splitting via prescribed rate loans and spousal RRSPs, capital gains planning, and charitable donations of appreciated securities.

-

Deferred compensation is a portion of an executive's earnings set aside to be received and taxed in a future year, allowing executives to manage when taxable income is triggered, often timed to lower-income periods like retirement.

-

An executive financial planner is a financial advisor who specializes in the complex compensation, tax, insurance, and estate planning needs of senior corporate professionals, coordinating strategy across all areas of an executive's financial life.

Key Takeaways

Executive compensation packages include base salary, RSUs, DSUs, LTIPs, and stock options, each with distinct tax implications that require proactive planning.

Deferred compensation structures allow executives to control when income is recognized, reducing taxable income in high-earning years.

RRSP and Individual Pension Plan contributions are among the most powerful tax deferral tools available to high-income earners in Canada.

Income splitting strategies, including prescribed rate loans and spousal RRSPs, can reduce the household’s overall tax burden when structured correctly.

Donating appreciated securities to a donor-advised fund eliminates capital gains tax and generates charitable tax credits.

Integrated executive financial planning coordinates tax strategy, deferred compensation, insurance, and estate planning under one roof.

A Plan That Keeps Up With Your Compensation

Executive financial planning isn’t a single conversation. It sits at the intersection of tax planning strategies, deferred compensation, insurance, and estate complexity, and the decisions made in one area create consequences in the others.

At Longevity Wealth, we work with C-suite professionals across Canada to bring structure, clarity, and strategy to the full complexity of executive compensation.

If your package has outgrown your current plan, a no-obligation discovery call is a good place to start.