How to Choose a Financial Advisor in Toronto

Image Source: Gemini 2026

Toronto's high-net-worth residents require a certified financial planner who can integrate tax, insurance, estate, and investment strategies into a single framework. This guide covers how to evaluate credentials, fee structures, and specialization focused on complex wealth management over generalists who rely on standardized templates.

For high-net-worth individuals in Toronto who have spent decades accumulating significant wealth, locating a suitable financial advisor can be an unexpectedly challenging endeavour.

Your financial landscape likely includes complex elements like an evolving estate, a robust investment portfolio, and retained earnings within a holding company. Despite your achievements, the financial planners at your current institution may lack the specialized expertise required to manage the intricacies of your current situation.

The Unique Requirements of High-Net-Worth Financial Planning in Toronto

The criteria for selecting a financial planner shifts dramatically once liquid investable assets reach the $1 million threshold. While many Canadians focus on foundational steps such as establishing emergency funds or opening RRSPs (registered retirement savings plans), high-net-worth individuals must navigate a multifaceted landscape of insurance structuring, corporate tax strategies, and complex retirement and estate planning.

Standard bank branch advisors are typically generalists and often lack the training to address such sophisticated needs.

If you have experienced the frustration of explaining your corporate structure to a bank advisor who doesn’t grasp its nuances, or if you are tired of being reassigned to new account managers who require multiple meetings just to understand your history, you already know the feeling.

This guide is designed to help you find a professional who matches your level of complexity.

Why Choosing a Financial Advisor in Toronto Is Different for High-Net-Worth Individuals

For most Canadians, choosing a financial planner is about getting started: building an emergency fund, opening an RRSP, and picking a mutual fund. For high-net-worth individuals, that conversation looks completely different.

Standard investment management is often insufficient once your liquid investable assets surpass $1 million. At this level of wealth, your financial needs become significantly more complex, requiring a simultaneous focus on corporate tax strategies, estate planning, insurance structuring, and retirement goals.

Because of this multifaceted landscape, a generalist advisor at a bank branch typically lacks the specialized training required to address such sophisticated requirements effectively.

And in Canada, anyone can legally call themselves a financial advisor. The title carries no regulatory protection at the federal level. In Ontario, however, the title of Financial Planner is legally protected, and anyone providing investment advice must be registered with the provincial securities regulator.

This distinction matters when you’re evaluating who’s qualified to manage the complexity of your financial situation.

Source: Canva

The Problem With Big-Bank Advice at This Level

The big banks serve millions of Canadians and do so reasonably well for straightforward financial situations. But when your needs involve a professional corporation, a holding company, or a liquidity event from a tech venture, the branch model starts to show its limits.

The most common frustrations we hear from prospective clients include:

Advisors who lack experience with incorporated professionals

No coordination between the tax side and the investment side

Frequent relationship turnover that forces you to re-explain your entire financial history every year or two

That’s not a financial plan. That’s triage.

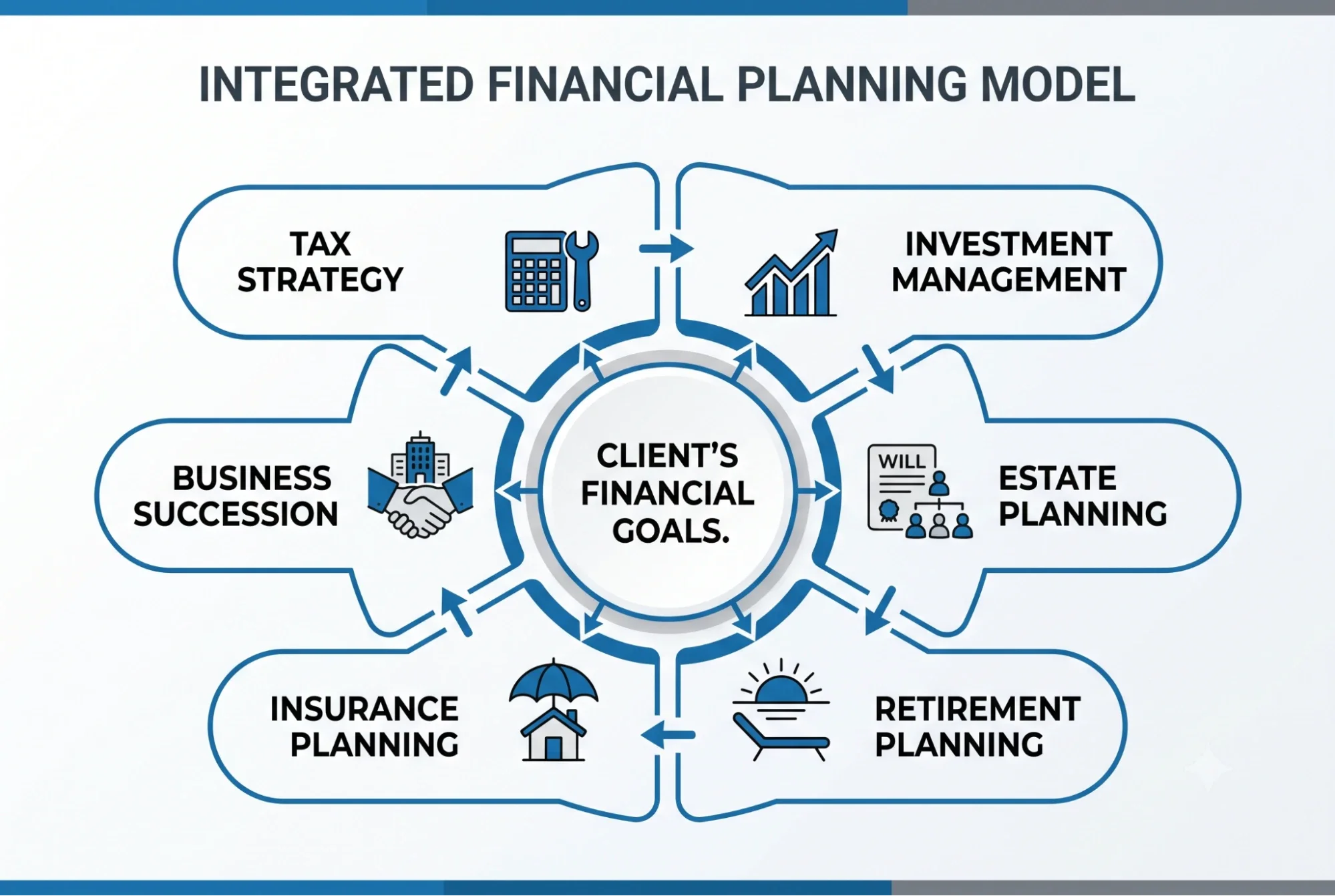

What Integrated Financial Planning Actually Looks Like

The alternative is a 360-degree advisory model that coordinates tax strategy, insurance, investing, estate planning, and alternative investments under one roof. Your advisor isn’t one of several disconnected professionals sending you contradictory guidance. They’re a single point of contact who understands the full picture and can build a comprehensive financial plan around your actual life.

This matters especially for incorporated business owners and C-suite professionals whose financial lives don’t separate neatly into personal and corporate buckets. A holistic approach to financial planning connects those layers and keeps your long-term financial goals in focus across all of them.

What to Look for in a Financial Advisor in Toronto

Not all financial advisors offer the same level of service, and asking the right questions up front will save you significant time.

Credentials and Designations

The Certified Financial Planner (CFP) designation is the most widely recognized professional standard in Canada. A certified financial planner is trained to take a holistic view of a client's financial situation, not just their portfolio, making it a meaningful credential for anyone with complex planning needs.

In addition to the CFP, the Registered Financial Planner (RFP) status is considered the premier benchmark for financial planning excellence in Canada. Specialized expertise, such as the Chartered Life Underwriter (CLU) designation, provides essential insights for estate and insurance planning, while a portfolio manager qualification is vital for those requiring discretionary investment management.

When searching for a certified financial planner in Toronto, verify credentials directly through FP Canada's public registry or the Canadian Investment Regulatory Organization's National Registration Search.

Anyone can claim to be a financial planner. Not everyone is accountable to a regulatory body.

Image Source: Gemini 2026

Fee Structure and Transparency

Understanding how your advisor is compensated is non-negotiable. The three most common payment models are commission-based, fee-based, and fee-only.

1. Fee Only

A fee-only financial planner in Toronto charges a flat fee or an hourly fee for their advice and does not sell financial products or earn commissions on the products they recommend.

This fee structure eliminates a significant source of potential conflict of interest, which is why many high-net-worth individuals actively seek out fee-only financial planning advice. It’s worth noting that fee-only financial planners are very rare in Canada, making up well under 1% of the advisory market.

2. Fee-based

Fee-based planners typically charge a percentage of assets under management annually, while commission-based advisors earn fees from the financial products they sell.

3. Commission-based

Commission-based advisors may be incentivized to recommend specific products, which is a meaningful distinction when evaluating objectivity. For context, Management Expense Ratios for mutual funds can exceed 2% in Canada, and commission-based advisors can charge over $20,000 annually on $1 million invested, costs that aren’t always visible upfront.

There’s no universally right fee structure, but transparency is the baseline. If your advisor can’t clearly explain how they’re paid, that’s a red flag.

Specialization in High-Net-Worth Planning

A financial planner who works primarily with incorporated professionals, C-suite executives, and business owners brings a fundamentally different level of expertise to the relationship than a generalist serving a broad range of clients at a financial institution.

Ask directly:

What’s the typical profile of your clients?

What percentage of your practice works with incorporated professionals or business owners?

How do you coordinate with a client's accountant or lawyer?

Do you provide a written, comprehensive financial plan, or is your advice ad hoc?

A quality financial advisor should never offer purely ad hoc advice. The answers to these questions will tell you quickly whether you’re being treated as a priority client or as one of many.

Source: Canva

What to Expect From a Financial Advisor in Mississauga and Toronto

The Greater Toronto Area has no shortage of advisors, but supply doesn’t equal quality. If you’re specifically looking for a financial advisor in Mississauga, the same criteria apply: credentials, fee transparency, and specialization, with the added benefit of local in-person access.

Many Toronto-based firms also serve clients across other provinces virtually, which matters if your business interests extend beyond Ontario.

What distinguishes a strong advisory relationship at the high-net-worth level isn’t proximity, but continuity.

The financial planner who has worked with you across multiple tax seasons, advised you through a corporate restructuring, and helped you coordinate your estate with your lawyer already in the room is worth considerably more than someone who manages investments and little else.

The Discovery Process

Any reputable financial advisor should offer an initial no-obligation consultation before asking you to commit to anything. This is your opportunity to assess fit:

Does this person understand my situation?

Do they ask the right questions about my financial goals and financial future?

Do they speak in plain language, or do they hide behind jargon?

Pay attention to whether the advisor listens first or pitches first. An advisor who opens by talking about their services before understanding your goals is showing you something important.

Tip: If you’re uncertain about your current advisory relationship, seeking a second opinion from an independent financial planner is always a reasonable step.

Red Flags to Watch For

A few things should give you pause, regardless of how polished the presentation is: financial planners who promise specific returns, advisors who can’t explain their fee structure, and planners who seem unfamiliar with the specific needs of your situation, whether that’s managing cash flow across a corporate structure, planning for retirement as an incorporated professional, or coordinating taxes across multiple entities.

Overpromising outcome language is both a regulatory red flag and a trust red flag. Strong advisors speak in terms of strategy, process, and expertise, not guaranteed results. If the conversation feels more like a sales pitch than a planning session, trust that instinct.

How Longevity Wealth Approaches Financial Planning in Toronto

Longevity Wealth is a Toronto-based wealth advisory firm serving Canadians with $500K or more in net worth, offering in-person meetings in Toronto and Mississauga and virtual access across Canada (excluding Quebec). For clients in other provinces, video conferencing makes the full advisory team accessible without sacrificing the quality of the relationship.

What sets the model apart is its fully integrated structure. Rather than referring clients out to external specialists, Longevity's team of certified financial planners, insurance specialists, portfolio managers, accountants, and estate planning experts work in coordination. Investment management is delivered through licensed portfolio management firms Bold Wealth and Proof Capital. Financial planning is embedded in the service model at no additional charge.

The relationship is long-term by design. Your dedicated advisor isn’t positioned across from you as a product provider; they’re a strategic partner who sits beside you, aligned with your goals, retirement timeline, business interests, and life.

If the wealth you’ve built has started to feel underserved by the team currently managing it, that’s not a small thing. It’s a signal worth acting on.

FAQs About Financial Advisors in Toronto

-

For high-net-worth individuals, yes. A coordinated financial plan covering taxes, retirement, estate planning, and insurance typically delivers far more value than the fees paid, especially compared to siloed advice from big banks.

-

Advisors who can’t clearly explain their fee structure, promise specific returns, or offer only ad hoc advice rather than a comprehensive written financial plan are significant red flags.

-

Costs vary by payment model. Fee-only planners charge a flat or hourly fee. Fee-based advisors charge a percentage of assets under management. Commission-based advisors earn fees from the financial products they sell, which can exceed $20,000 annually on $1 million in assets.

-

Many full-service financial planners in Toronto work with clients with net worths of $500,000 or more. At that asset level, integrated planning covering taxes, insurance, and investing typically delivers meaningful long-term value.

Key Takeaways

In Canada, anyone can call themselves a financial advisor, so always verify credentials through FP Canada or the Canadian Investment Regulatory Organization before committing.

The Certified Financial Planner (CFP) and Registered Financial Planner (R.F.P.) designations represent the highest standards in Canadian financial planning.

Less than 1% of Canadian financial planners are fee-only; rare, but the gold standard for conflict-free financial planning advice.

High-net-worth individuals need a financial planner who coordinates taxes, insurance, investing, and estate planning under one roof, not siloed advice.

Always ask how your advisor is paid, as commission-based advisors may be incentivized to sell specific financial products rather than those that better serve your goals.

A no-obligation discovery call is the right first step when evaluating a new financial advisor in Toronto or Mississauga.

Ready to Find a Financial Planner Who Understands Your Situation?

Choosing the right financial advisor in Toronto is one of the highest-leverage decisions a high-net-worth individual can make. The wrong fit costs more than fees. It costs time, missed opportunities, and the ongoing frustration of financial planning advice that doesn’t talk to itself.

Longevity Wealth offers a no-obligation discovery call for prospective clients looking to understand what a truly integrated advisory model looks like for their specific situation. If your financial life has grown beyond what your current advisor can address, our financial advisors in Toronto are a good place to start.

Book a no-obligation discovery call and start the conversation toward financial planning built around your entire life and not just your portfolio.